Late last year, we warned you about The End of Cheap Phones. We detailed how a devastating global memory chip shortage and rising processor fabrication costs would add up to KES 9,100 to the retail price of your next device. But as we move deeper into 2026, a much darker reality is emerging from the supply chain data: this is no longer just about you paying more. It is about whether your favourite budget smartphone brand will even exist by 2027.

Recent intelligence from Counterpoint Research reveals a stark divide in the industry. The skyrocketing costs of Bill of Materials (BOM) are pushing the entry-level smartphone market to the brink. While premium giants will casually pass the “AI Tax” onto consumers, budget manufacturers face a brutal dilemma: shrinkflation, massive price hikes, or a complete exit from highly competitive markets.

The Root Cause: The “Maize vs. Specialised Coffee” Crisis

To understand why a company like Infinix or itel is currently sweating, you have to look past the marketing jargon and understand the raw mechanics of the global silicon supply.

Imagine global chip production as a massive agricultural estate. For years, tech giants dedicated 90% of their land to growing everyday maize; the standard DRAM and NAND memory chips used in billions of affordable Android phones. Only a tiny fraction of the land was reserved for highly specialised, ultra-expensive “coffee beans”; High Bandwidth Memory (HBM) used in enterprise servers.

Then the AI boom exploded. Cloud operators and AI firms started offering astronomical sums for that specialised coffee. The mega-farmers (Samsung, SK Hynix, Micron) realised the profit margins were too good to ignore. They ripped up their maize fields to plant more coffee. Consequently, there is now a severe global shortage of everyday smartphone memory, and prices for standard DRAM have surged by over 30% since early 2025.

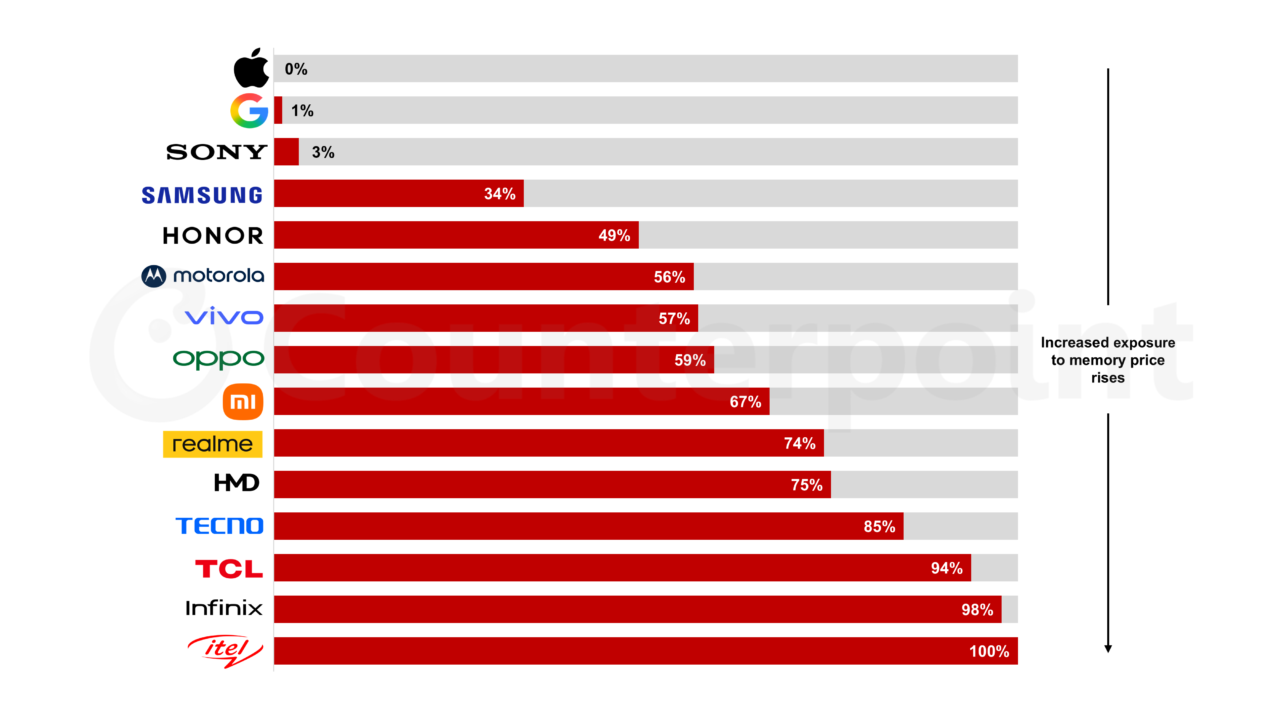

The Danger Zone: Exposure to the Sub-KES 32,260 Market

This memory squeeze does not impact all brands equally. According to Counterpoint’s latest breakdown of European and global market exposure, the crisis heavily targets the sub-$250 (roughly KES 32,260) wholesale market. In this bracket, margins are non-existent, and consumers are fiercely loyal to their wallets, not the brand logo.

We can divide the smartphone ecosystem into three distinct survival tiers:

- The Insulated Elite (0% – 3% Exposure): Apple (0%) and Google (1%) do not play in the budget sandbox. Because they dictate the premium market, they don’t absorb the rising costs, they just creatively pass them onto the consumer. We’ve just seen this executed flawlessly with the new Apple M5 Mac refresh. Apple quietly killed off the beloved sub-KES 130,000 ($999) MacBook Air, forcing the new base model to start at roughly KES 148,000 ($1,099). To mask the price hike, they simply doubled the base storage to 512GB.

- The Cross-Subsidised Giants (34% – 67% Exposure): Brands like Samsung (34%), motorola (56%), and Xiaomi (67%) have broad portfolios. Samsung is employing the exact same “Stealth Tax” strategy as Apple. For their 2026 flagship phone launch, they quietly bumped the entry price of the base Galaxy S26 from $799 to $899 by killing off the 128GB tier. The massive profits these giants rake in from forced premium upgrades heavily subsidise the bleeding in their budget divisions.

- The Existential Threat (74% – 100% Exposure): This is the red zone. Transsion brands, which have historically dominated the Kenyan value-for-money segment, are heavily exposed. TECNO relies on this budget bracket for 85% of its volume, Infinix sits at a dangerous 98%, and itel is 100% exposed. When memory chips suddenly cost 30% more, the profit margin on a KES 15,000 device is instantly obliterated.

Tactics of Desperation: Shrinkflation vs. Extinction

There is a brilliant, yet brutal juxtaposition in how the tech industry is handling 2026. Premium brands force you to pay more by upgrading your base storage. Budget brands, however, cannot force a customer with a strict KES 20,000 budget to suddenly spend KES 30,000.

Jan Stryjak, Associate Director at Counterpoint, bluntly noted that he “would not be surprised if the European smartphone market has one or two fewer players once we exit the tunnel.”

To survive until the memory market corrects itself (projected for H1 2027), highly exposed brands are deploying desperate tactics. The most insidious of these is shrinkflation. Instead of raising the retail price, manufacturers will quietly downgrade the internal specifications. You might pay the exact same KES 22,000 you paid in 2024, but instead of 8GB of fast RAM and 256GB of storage, you will unbox a device hobbled with 4GB of RAM and slower, older storage chips.

Editor’s Take

The golden era of the ultra-cheap, over-specced smartphone is dead, killed by the global pivot to AI. The 2026 market will act as a ruthless Darwinian filter. Massive conglomerates will weather the storm by executing stealth price hikes, but smaller or budget-reliant manufacturers face a grim reality: consolidate, hike prices, or die.

For the Kenyan buyer, the advice we gave in December still stands, but with a heavier warning. If you are shopping in the sub-KES 30,000 category this year, you must read the spec sheets with a magnifying glass. Do not assume the 2026 version of a phone is better than the 2025 version. In the age of hardware shrinkflation, buying last year’s model, or hunting for a refurbished premium device, is no longer just a clever hack; it is the only way to avoid being shortchanged.