Diamond Trust Bank has rolled out a range of NFC-enabled wearables that let customers pay by tapping a ring or silicone wristband at any compatible point-of-sale terminal. The collection is now live on a dedicated catalogue at wearables.diamondtrustbank.co.ke. It is DTB’s first proper push into wearable banking hardware.

And if you look at it carefully, there is something clever hiding in plain sight. These devices completely sidestep Apple’s infamous NFC restrictions.

What DTB is actually selling

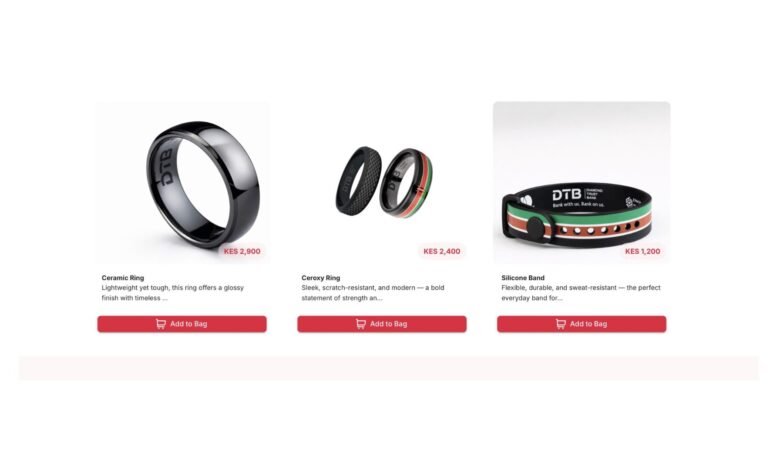

Three items are on the catalogue right now.

The Silicone Band sits at KES 1,200. It is a flexible, sweat-resistant strap in black with a Kenyan flag pattern running through it. It looks like a fitness band, which is very likely the point.

The Ceroxy Ring retails at KES 2,400, with two pattern options: Kenyan flag, and carbon fibre. Available in sizes 8, 10, and 12.

Make tech-ish your favourite news source

Star tech-ish.com on Google. We move up your daily feed.

The Ceramic Ring is the premium option at KES 2,900, also in sizes 8, 10, and 12. Glossy black finish. It reads as fashion jewellery rather than banking hardware.

All three link to a customer’s existing DTB debit card and are powered by Tappy Pay, the wearable payments provider DTB brought on board through its Mastercard partnership.

Why the Apple problem stopped mattering

This is the subtle part worth pausing on.

When Safaricom recently confirmed M-Pesa Tap-to-Pay is coming to Kenya, one of the immediate concerns was that iPhone users would be locked out. Apple restricts NFC access to Apple Pay only. No third-party wallet, including M-Pesa, can tap through an iPhone’s hardware. Android users get the feature. iPhone users do not.

DTB’s wearables ignore that problem entirely. The ring or band does not depend on your phone. It is the payment instrument. Whether you carry an iPhone, a Tecno, or no phone at all, you tap the device and it works. That is a meaningful advantage, particularly in a market where iPhone users tend to be the high-value banking customers DTB is specifically chasing.

How it actually works

NFC, or Near Field Communication, is a short-range wireless technology that lets two devices exchange data when they are within a few centimetres of each other. Contactless card payments have used it for years.

DTB’s wearables use the same underlying technology. The chip simply lives in a ring or a band instead of a plastic card. Tappy Pay’s platform handles tokenisation, which means your actual card number is never stored on the device. Instead, a unique encrypted token stands in for each transaction. Even if a merchant’s terminal is compromised, your real card details are not exposed.

According to TechArena, transactions are capped at KES 5,000 per tap and KES 10,000 per day. That cap is the main practical constraint. It is fine for coffee, matatu fare, supermarket runs, and petrol top-ups. It is not designed for large purchases.

If you lose the device, you can suspend or permanently deactivate it through the Tappy Pay app. There are no extra fees beyond the normal card charges that already apply to a DTB debit card.

Kenya has been here before

Safaricom attempted wearable payments back in 2017 with M-Pesa 1Tap, a combination of wristbands and NFC stickers piloted in Nakuru. That product is now defunct. Safaricom has since shifted its contactless strategy toward smartphone-based tap-to-pay.

DTB is therefore not pioneering wearables in Kenya. It is the first Tier One bank to do it. That distinction matters because banks operate on card rails. A DTB wearable works globally at any contactless-enabled terminal. A 1Tap wristband only worked within M-Pesa’s closed merchant network.

This continues a pattern we saw with AbsaPay in 2024, when Absa Kenya turned the Android smartphone into a tap-to-pay instrument. Banks are systematically removing the friction between a customer’s card and the point of sale. Wearables are simply the next layer.

The catch

A few things worth being clear about.

You must already be a DTB customer with an active debit card. These wearables are not standalone accounts.

The KES 5,000 per transaction ceiling means this is strictly a small-ticket instrument. You will not be buying a fridge with a tap of your ring.

Adoption depends on contactless-enabled POS terminals. Common in urban supermarkets, petrol stations, and chain restaurants. Still patchy in smaller outlets and rural areas.

DTB has also not publicly detailed what happens if your ring is stolen and used up to the daily limit before you suspend it. The Tappy Pay FAQ says you can lock the device through the app, but the liability framework for no-PIN contactless payments in Kenya is not yet transparent.

What this signals

DTB is coming off a strong year. It posted KES 10.7 billion in profit and grew its customer base by 45% in 2025. Launching a visible, lifestyle-oriented product like payment jewellery is an obvious play for retail visibility among younger and urban customers who have plenty of banking options.

The deeper question is whether wearable payments finally stick this time. The technology is mature. The partnerships are solid. And critically, wearables are the only contactless payment method that completely bypasses the Apple and Google duopoly.

If adoption is slow, it will not be the product’s fault.

Join the discussion