As Safaricom pushes toward its new My OneApp future, one of the more interesting things I’ve seen tucked inside the current M-PESA app is a mini app called nesti. It is not the flashy kind of launch that grabs attention the way a super app demo does, but after digging through it myself, I think nesti may quietly be one of the more practical ideas Safaricom has put in front of ordinary users in a while.

The pitch is simple: pay your rent through nesti, and those payments help build a RentScore, which the service describes as a financial identity based on how consistently and reliably you pay over time. In a market like Kenya, where many people, especially freelancers, gig workers, and self-employed users, may not have a traditional payslip to present to lenders, that idea makes immediate sense to me.

From the onboarding screens, nesti is clearly positioning itself as a bridge between rent and financial access. One welcome page says your rent should count for something, and another goes even further by promising a “financial score that banks trust” with every rent payment. That is ambitious language, but the core idea is compelling. Rent is already one of the biggest recurring expenses for many people. If that behavior can be turned into a usable financial signal, that is a smart reframing of data people are already generating every month.

My walk through the mini app shows that Safaricom and its partners are trying to make the setup relatively straightforward. Signing in through M-PESA asks users to share their first name, last name, and mobile number. After that, nesti collects profile details including email, gender, date of birth, and phone number.

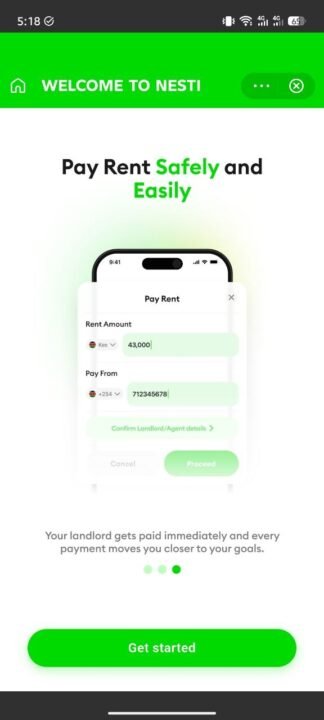

Users then add rental information such as location, monthly rent amount, and payment method, with support for M-PESA and bank transfer. Under the M-PESA route, the app allows rent payments to a paybill, till number, or phone number, which is important in Kenya because landlords and agents use all three methods depending on how formal or informal the setup is.

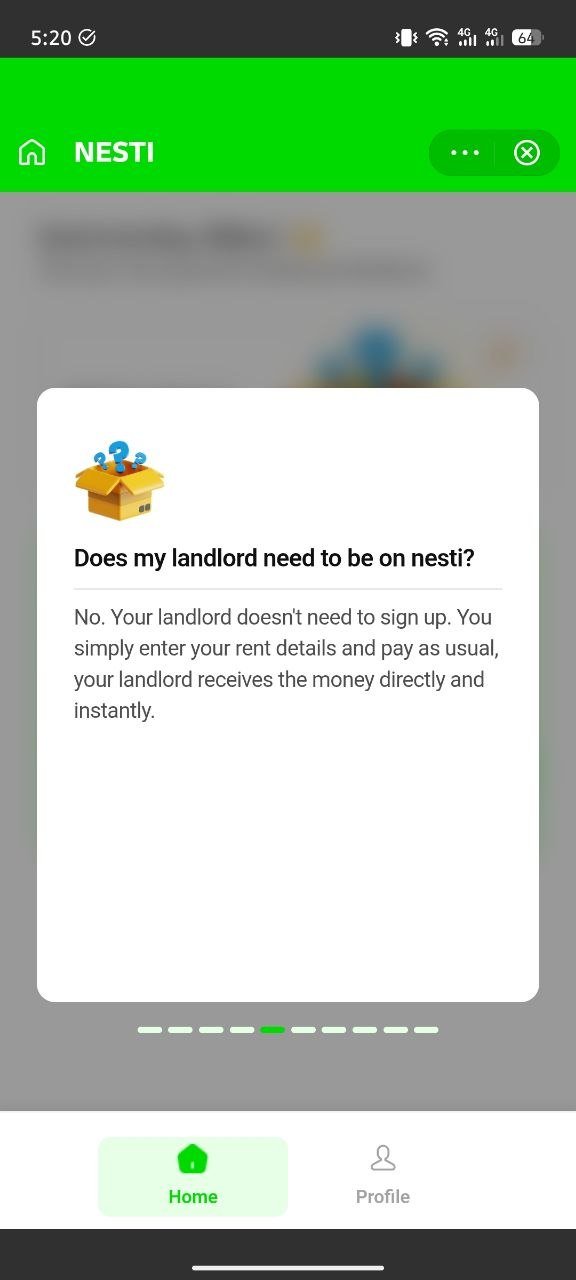

The app also asks for landlord or caretaker details, although it says those are optional and mainly help with sending rent receipts. That part stood out to me because it suggests nesti is trying to sit on top of existing rent habits, not force landlords into a new platform. In fact, one of the FAQ cards makes that even clearer: your landlord does not need to be on nesti. You just enter the rent details, pay as usual, and the landlord receives the money directly and instantly.

That frictionless part matters. In Kenya, anything that requires both tenant and landlord to fully onboard before it becomes useful usually dies a slow death, because humans enjoy turning simple things into logistical theatre.

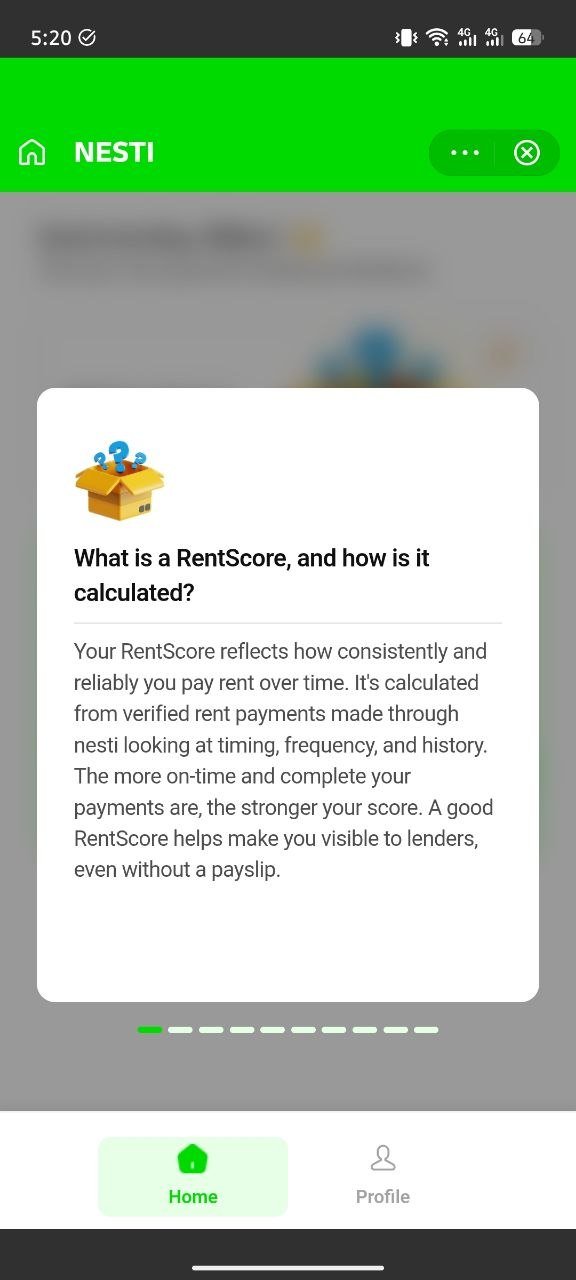

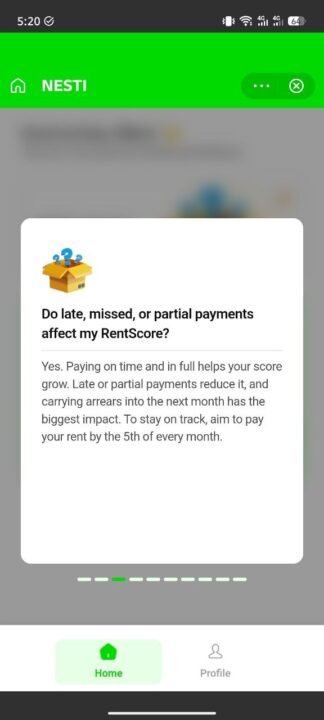

The FAQ section also gives a better sense of how the score works. According to nesti, RentScore is calculated from verified rent payments made through the app, looking at timing, frequency, and payment history.

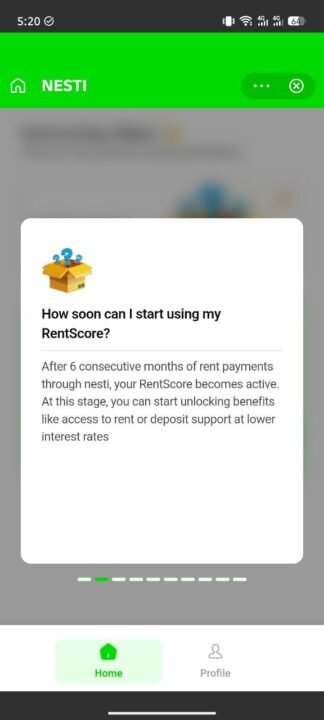

Paying on time and in full grows the score, while late, partial, or missed payments reduce it. Carrying arrears into the next month has the biggest impact, and the app even nudges users to aim to pay by the 5th of every month. After six consecutive months of rent payments through nesti, the RentScore becomes active.

That timeline is important because it shows this is not meant to be an instant-credit shortcut. It is more of a behavior-based credibility layer built gradually over time. For me, that makes the proposition feel more serious.

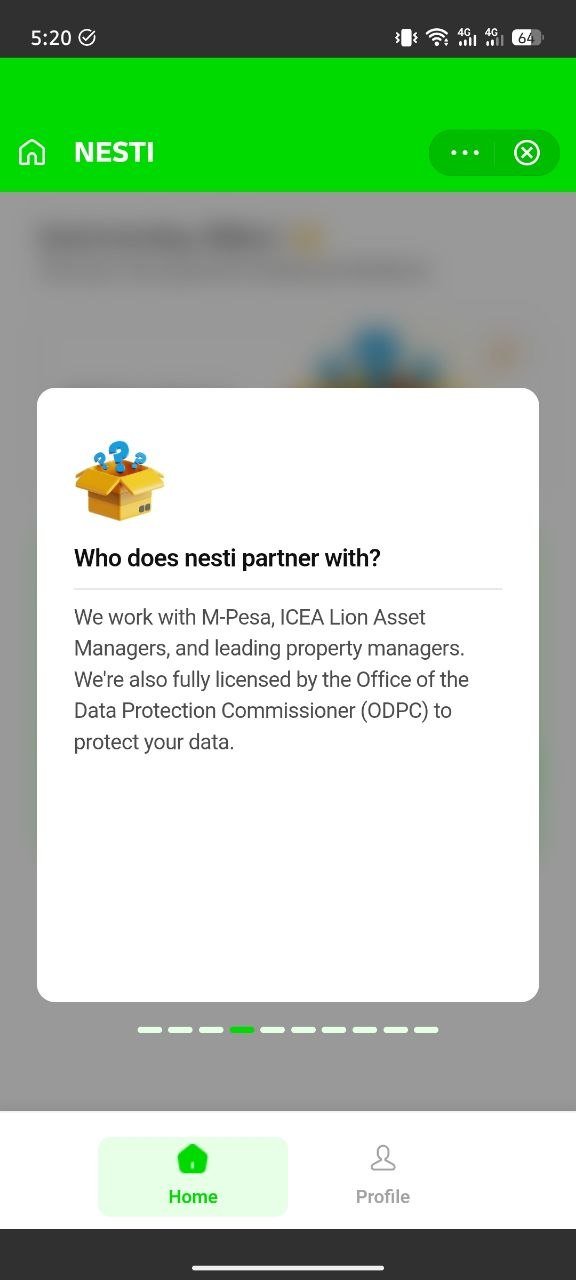

What also makes nesti worth watching is the partner list and the roadmap. The app says it works with M-PESA, ICEA Lion Asset Managers, and leading property managers, and it also highlights ODPC licensing around data protection.

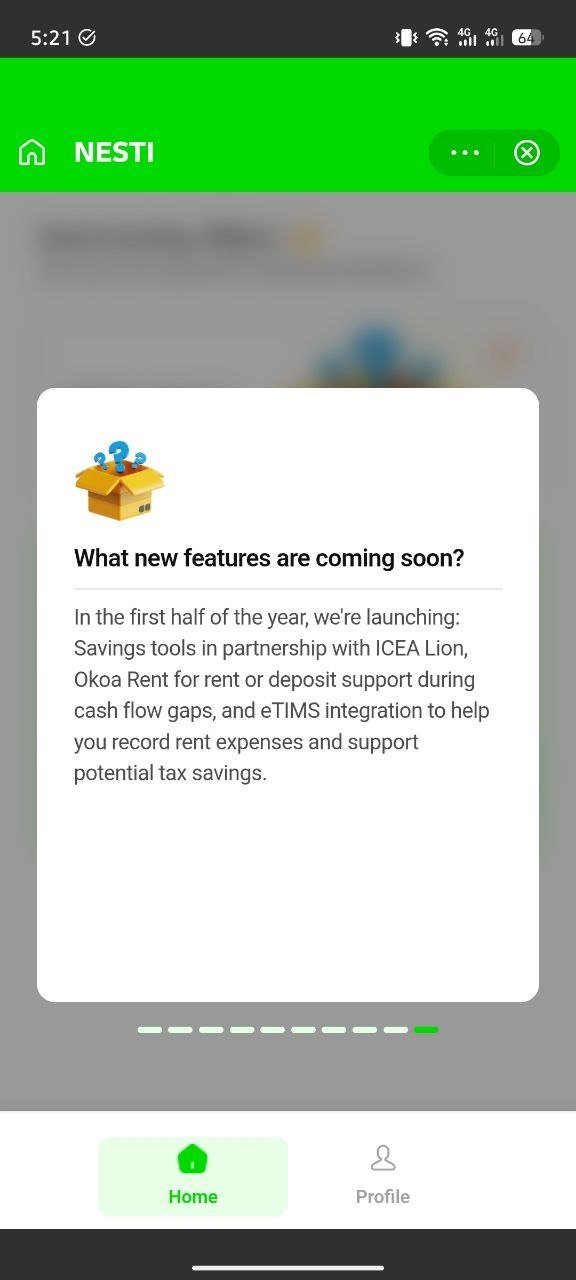

Future features planned for the first half of the year include savings tools with ICEA Lion, Okoa Rent for rent or deposit support during cash flow gaps, and eTIMS integration to help users record rent expenses and potentially support tax savings.

That future roadmap is where nesti starts to feel bigger than a simple rent tracker. Safaricom appears to be building a service that could sit at the intersection of payments, savings, credit visibility, and even housing access.

From where I sit, as someone who works independently and does not fit neatly into the traditional salaried template, this is exactly the kind of product I would keep an eye on. If it works as advertised, nesti could turn something I already do every month, pay rent, into something financially useful beyond just keeping a roof over my head. And that is what makes it interesting: not because it reinvents rent, but because it tries to make rent finally count.