My initial title was how to get your financial sh*t together. But seeing as the royal wedding was just this weekend, we shall maintain decorum and mind our language.

So another work week! It’s end month and you’re really anticipating your salary/ income. You’re drowning in bills and debt and its been a rat race month after month. 2018 was supposed to be the year of reckoning! Maybe that’s why you’re here, because you can’t imagine this is how the rest of your life looks like.

I did a quick poll on social media to make sure this article addresses what really affects us as youth. The major FAQs were:

- How does one budget and stick to it?

- How does one manage debt?

- How does one save towards a financial goal like starting a business or owning an asset?

- What are the best investments choices for young people to look into?

Here’s a quick step by step guide that may aid you out of the hole you dug yourself in.

Phase I: Clean up

Investigate

For those that love collecting receipts, this is your moment to shine! The only way to understand where your money is going is looking at how you’re spending it. Group the receipts in appropriate categories. You can also look at MPesa or bank statements. Take note of small details like withdrawal or convenience fee for debit cards. When personally taking this exercise I realised all my money tends to go towards cravings. I’ve accepted the possible fact I may be a junk food black hole. And there was once a scenario where using my card for a taxi service cost me a convenience fee of Ksh. 250!

Make tech-ish your favourite news source

Star tech-ish.com on Google. We move up your daily feed.

Financially aware

I would easily call this budgeting but most of you would zone out. Becoming financial aware means knowing how much debts, assets and income you own. Which brings us to debt management. List out your debt. All of it, even the 10 bob for the mama mboga. Upcoming expenses can also be included here in a similar format.

Prioritise urgency for those with approaching deadlines or you could arrange them from the most outstanding to the least and make realistic deadlines to clear them. This is where you approach those you owe and inform them that you will pay up on a certain date. Even if its a bank or Platinum creditors, restructuring loans would be better than dodging their calls, because at the end of the day they just want their money back. For more details on this check this previous article.

Net Worth

Next up is calculating your net worth. Yes, you can do this, it’s not just for rich old people. List the assets you own and their value: devices and investment policies count but not inheritance. Subtract the total debt you calculated from your total net worth.

This is basically your ground zero! Your starting point.

Income vs Expenses

Now lets look at your income. How much are you raking in and at what frequency?

Now look at how much your living expenses are either monthly or weekly depending on your income frequency, i.e. rent, fare/car payments,utilities, food, insurance. This gives you a visual of approximately how much you need to stay afloat. Please note expenses should be less than your income. If its higher, you now know why you’re suffering.

Phase II: Systems

I’ll term this segment as the financial diet. The work wasn’t in the lists in the above section, it’s actually in this phase; where you’re actually acting on the information.

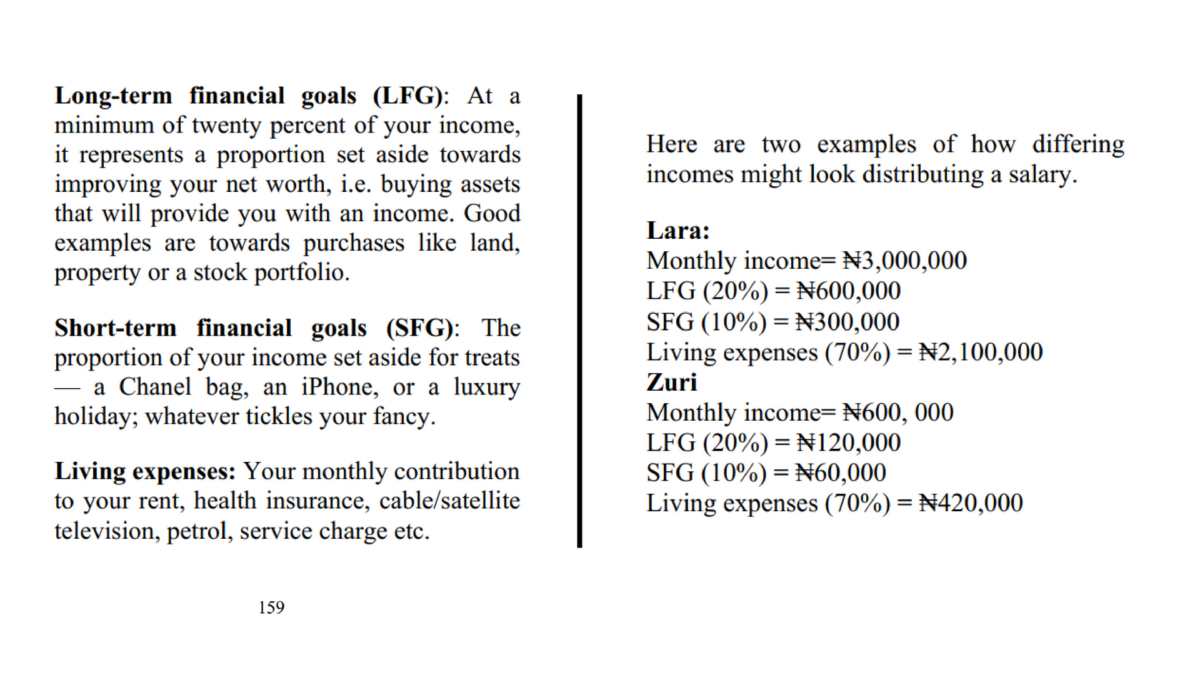

It’s important to distribute your salary to at least 4 accounts: Living expenses, Short term goals, Long term goals and Leisure. It would be best to automate the distribution or payments to prevent spending beyond the set budget. Here are excerpts from a book you’ll love called The Smart Money Woman by Arese Ugwu (Buy from Amazon):

Living expenses

This account collects exactly that. Do not withdraw or tamper with it. Personal finance requires a lot of grit and discipline. Don’t shrug it off with the insane notion that you’ll receive your salary/ still have a job next month.

Short Term Goals

This includes assets you’d like to purchase in the short term. A new phone, a laptop, a short vacation out of town. Be realistic with these goals especially if you’re in debt put it off till you clear money owed.

Long Term Goals

This refers to larger purchases/ investments but we’ll discuss this further in the next phase.

Leisure

Set aside a certain amount each month for leisure activities with family, friends or your significant other. By setting a specific amount consistently, you’ll gamble on your priorities better because being out today means you skip next week’s roadtrip or a movie night out. This way you won’t aimlessly give in to your impulse spending because there are consequences.

At first it will be really difficult but just be resilient and you’ll eventually get used to it and your money will seem surplus, which brings us to the next phase.

Phase III: Building wealth

As youth, we feel that saving for retirement is futile. I mean it’s so far away. Well our YOLO lifestyle is a fallacy and y’all better wake up and smell the coffee. These years of our youth are like smoke and this is the best time to learn how to build wealth which will go a long way.

Emergency fund:

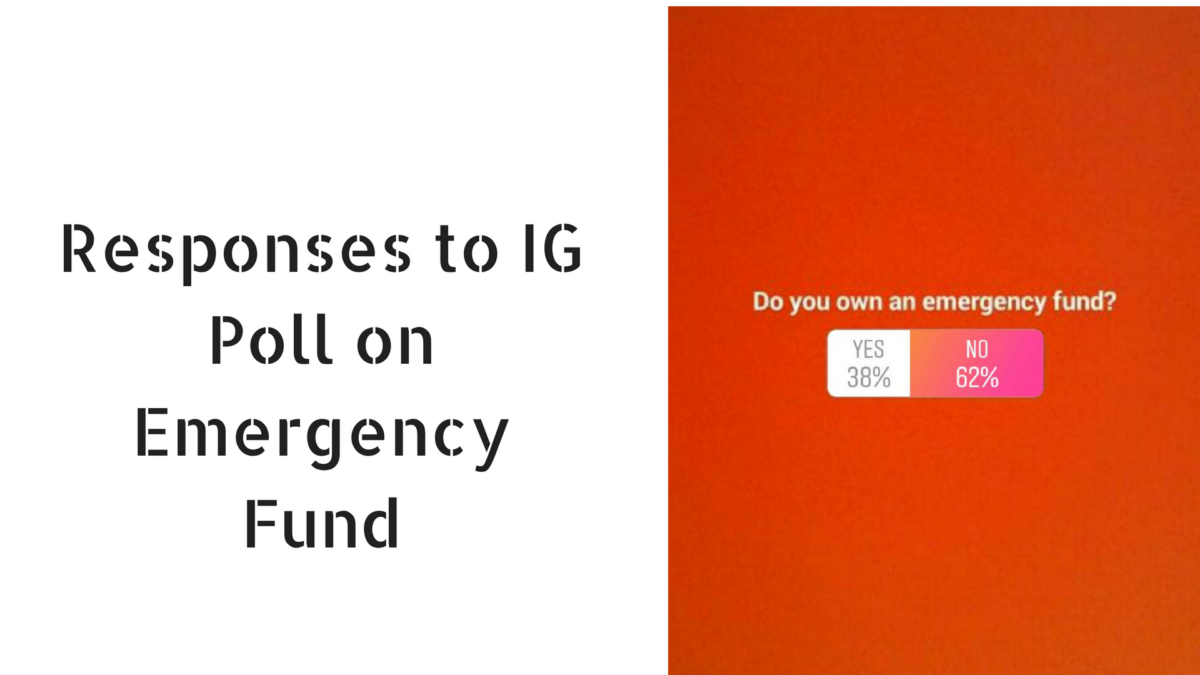

Before we proceed, please note this significant item. An emergency fund is very different from an insurance policy. The latter is money a company pays out to an institution for your medical care or damages. The former refers to a cushion that helps you absorb the shock of losing a job or your source of income. Your emergency fund should basically be 3 to 6 months of your living expenses. This prevents you from starting from square 1 when your foundation crumbles. This poll I took on Social Media shows only 38% of the 100 who answered have an emergency fund.

Now that that’s out of the way, let me point out that a long term goal account can be as little as 20% of your income every month. Say you’re earning Ksh. 50,000 that’s Ksh. 10,000 which is a lot if you’re consistent for 2 years. .

You need to make another list, but this one is fun. Write out what you’d like to own and be specific; a 3 storey mansion, an acre in Kamulu or a red 2016 Mazda demio. Research on value and appreciation because an asset that doesn’t gain value over time is just another liability. If it’s land look at the property tax and land rates. Be smart about it. Once you’ve made this list, approach any Asset Finance Bank or Insurance Company that sells different investment policies and deliberate on which one you want to pick.

You can look at the very well detailed investment elaborations on Stocks, Real Estates, Mutual Funds, and Treasury Bills from The Smart Money Woman book by Arese Ugwu to better understand which you would want.

With these explanations in mind and being fully aware of your individual financial goals, take time to speak to an agent. I personally invest with Old Mutual since I was 18. Make sure you try and speak to the same agent because rapport is crucial when you delay on a payment. Also do your own research, learn trends if you want to invest in stock and be open with your agent. Try have a diversified portfolio and avoid investments with high risk of losing the invested amount.

Warren Buffet: Be fearful when others are greedy but greedy when others are fearful.

Find out from your investment advisor:

- The best investment strategy (depending on financial goals and timelines)

- Risk

- Profitability

- Liquidity

- Tenor (lock in period and penalties for defaulting on contract terms)

Building wealth helps in improving the value of your net worth. Being financially free, doesn’t happen overnight.

I do hope you will bookmark this page because all this information was put together just for you. Thank you everyone who engaged with me on my inquiries on social media(Major appreciation)

Do you have any questions or items you’d like to be clarified? Feel free to comment or reach me on my twitter handle @sndutah

Lovely tips, this is a forsight article

i really hope youth can especially adhere to this